![]()

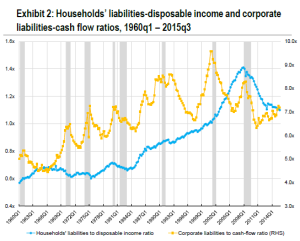

Using the dynamics of credit–which most other economists ignore–I explain why Japan, the USA and UK are among the “Walking Dead of Debt” and why China, Canada, Australia and South Korea are on their way to joining the Debt Zombies. This presentation is based on work I’m doing for a new 25000 word book for Polity Press entitled “Can we avoid another financial crisis?”, which should be published later this year.