![]()

In the previous post, I outlined my basic model of a pure credit economy, in which a single initial loan allowed a continous flow of economic activity (at a constant level) over time. The basic flowtable of that system was:

| Type | 1 | -1 | -1 | -1 |

| Account | Firm Loan (FL) | Firm Deposit (FD) | Bank Deposit (BD) | Worker Deposit (WD) |

| Interest on Loan | +A | |||

| Interest on Deposit | +B | -B | ||

| Pay Interest on Loan | -C | -C | +C | |

| Pay Wages | -D | +D | ||

| Interest on Deposit | -E | +E | ||

| Consume | +F+G | -F | -G |

The next stage of the model allows for repayment of loans, and re-circulation of these repayments. For this, another account is needed: a capital account that records the inactive reserves of the banking system–those reserves the banking system has available for lending. The two additional steps that are considered now are:

- The firm pays money to the bank that is to be taken off its outstanding debt. This is a transfer of H from the firm’s deposit account to the bank’s capital account, and in recognition of receiving it, the bank is olbiged to reduce the recorded amount of outstanding debt by the same amount; and

- The bank can now re-lend existing inactive reserves to firms. This is a transfer of money I from the bank’s capital account to the firm’s deposit account, and in recognition of having given it to the firm, the bank records that the firm’s debt has risen by the same amount.

Adding these new flows to the table generates the following system:

| Type | 1 | 0 | -1 | -1 | -1 |

| Account | Firm Loan (FL) | Bank Reserves (BR) | Firm Deposit (FD) | Bank Deposit (BD) | Worker Deposit (WD) |

| Interest on Loan | +A | ||||

| Interest on Deposit | +B | -B | |||

| Pay Interest on Loan | -C | -C | +C | ||

| Pay Wages | -D | +D | |||

| Interest on Deposit | -E | +E | |||

| Consume | +F+G | -F | -G | ||

| Repay Loan | -H | +H | -H | ||

| Relend Reserves | +I | -I | +I |

This is still an equilibrium system–though it operates at a lower level than the previous one where a single injection of credit money circulated indefinitely, because there is less money in active circulation. The next step–and the one that explains how money can expand endogenously–is to introduce the creation of new credit money. The mechanism is extremely simple. As Basil Moore, the pioneer of “endogenous money” theory, argued decades ago, major firms have “lines of credit” that enable them to increase their spending at will, in return for accepting a matching increase in their debt levels. In a growing economy, these “lines of credit” (and their domestic equivalent, the gap between aggregate credit card balances and aggregate limits) are growing all the time.

In this simple model, this simultaneous expansion of both debt and money is captured by the sum J being added to the firm’s deposit account, in return for the bank adding the same sum to the outstanding debt of the firm.

| Type | 1 | 0 | -1 | -1 | -1 |

| Account | Firm Loan (FL) | Bank Reserves (BR) | Firm Deposit (FD) | Bank Deposit (BD) | Worker Deposit (WD) |

| Interest on Loan | +A | ||||

| Interest on Deposit | +B | -B | |||

| Pay Interest on Loan | -C | -C | +C | ||

| Pay Wages | -D | +D | |||

| Interest on Deposit | -E | +E | |||

| Consume | +F+G | -F | -G | ||

| Repay Loan | -H | +H | -H | ||

| Relend Reserves | +I | -I | +I | ||

| Extend Credit | +J | +J |

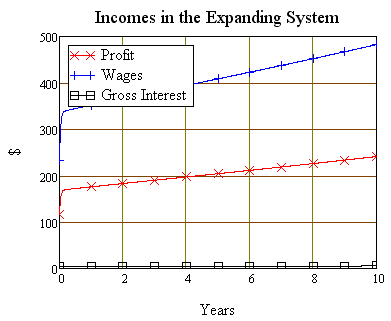

With this extension, we move out of the realm of equilibrium–so long as J is positive, the money supply and the economy will be expanding (we also comprehensively invalidate “Walras’ ‘Law’ ”, a cornerstone of neoclassical economics–but that’s a topic for a later post). Starting from the equilibrium values of the previous system, the bank balances and incomes in the system grow as indicated by the next two graphs.

All the models so far describe “well behaved” financial systems: the banks make their money out of the spread between loan and deposit rates of interest (other extensions cover non-bank lending, which is part of the explanation of why debt exceeds money; but that’s another topic in itself). Next we introduce a badly behaved financial intermediary: one that pretends to make more money than the others, but in reality makes none at all–a Ponzi Scheme.

This is enough for one post; to be continued in Ponzi Maths–Part 3.